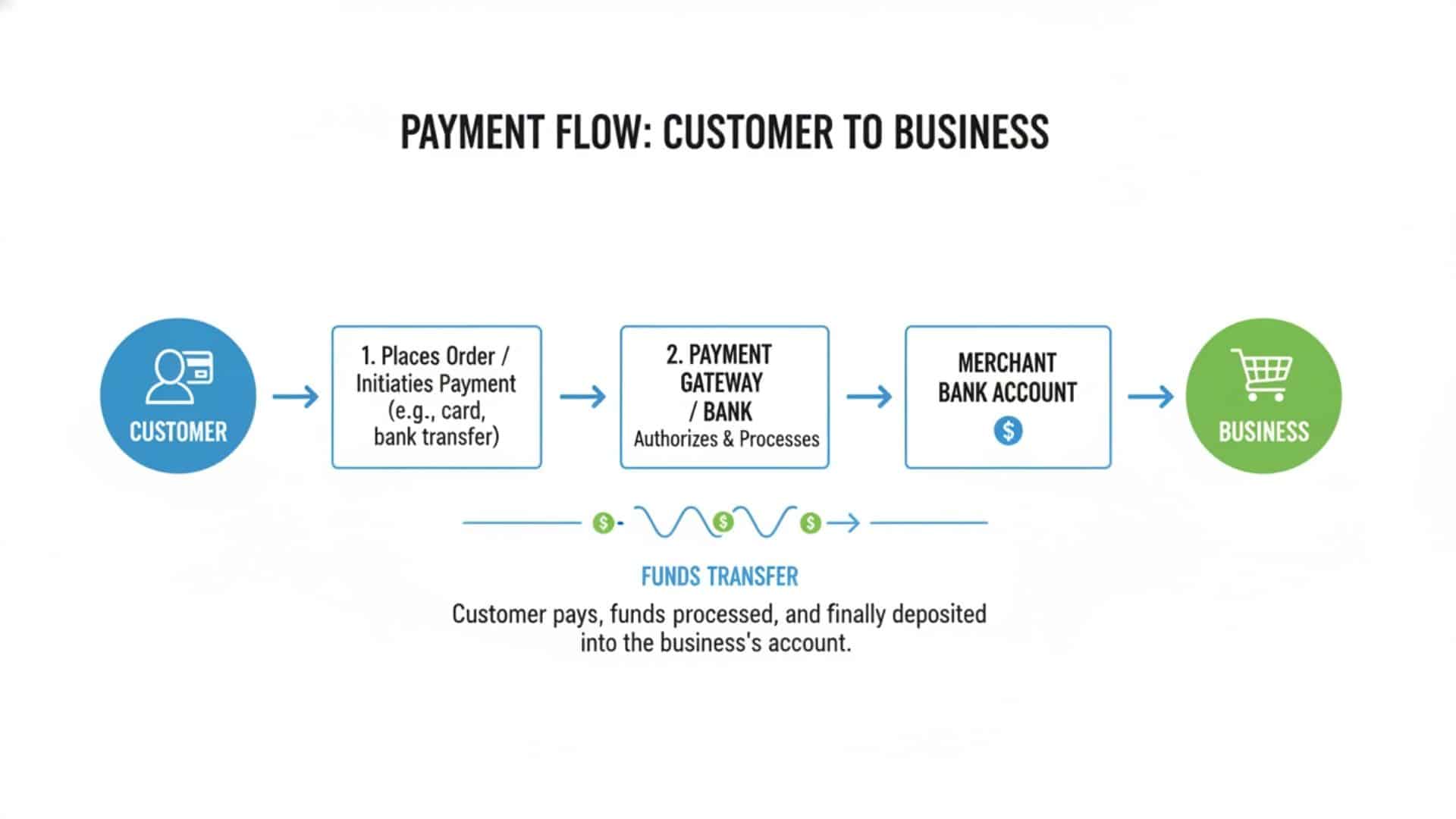

Choosing the right online payment setup can make a real difference for a small business. Customers want fast and secure ways to pay.

Business owners need low fees, a simple setup, and a steady cash flow. That is why it helps to compare your options before committing to one system.

This blog breaks down the best online payment methods for small businesses. You will find fee details, security tips, and a clear guide to choosing what best fits your business.

In this blog, I’ll show you how to set up payments that work for both your customers and your bottom line.

What Are Online Payment Methods for small businesses?

Online payment methods are the ways customers send money to you over the internet. Knowing the difference between key terms helps you make smarter decisions from the start.

- Payment method: How a customer pays, card, wallet, or bank transfer.

- Payment gateway: Software that securely sends payment data between your site and the bank.

- Payment processor: The company that moves funds between the customer’s account and yours.

These three work together in every online transaction. Offering multiple methods also matters for conversions. When a customer does not see their preferred payment option at checkout, they often leave.

PRO TIP: The more flexible your checkout, the more sales you are likely to close.

Why Small Businesses Need Multiple Payment Options

Payment flexibility is no longer a bonus. It is something customers expect when they shop online.

Most customers decide to leave a checkout page within seconds. If they do not see their preferred payment option, they move on. That is a lost sale you may never recover.

Different customers also trust different tools. Younger shoppers often prefer digital wallets. Older customers may stick with cards or direct bank transfers.

Service businesses and freelancers need invoice-based options that most e-commerce stores do not offer. Matching your payment options to your customer base directly affects how much revenue you collect each month.

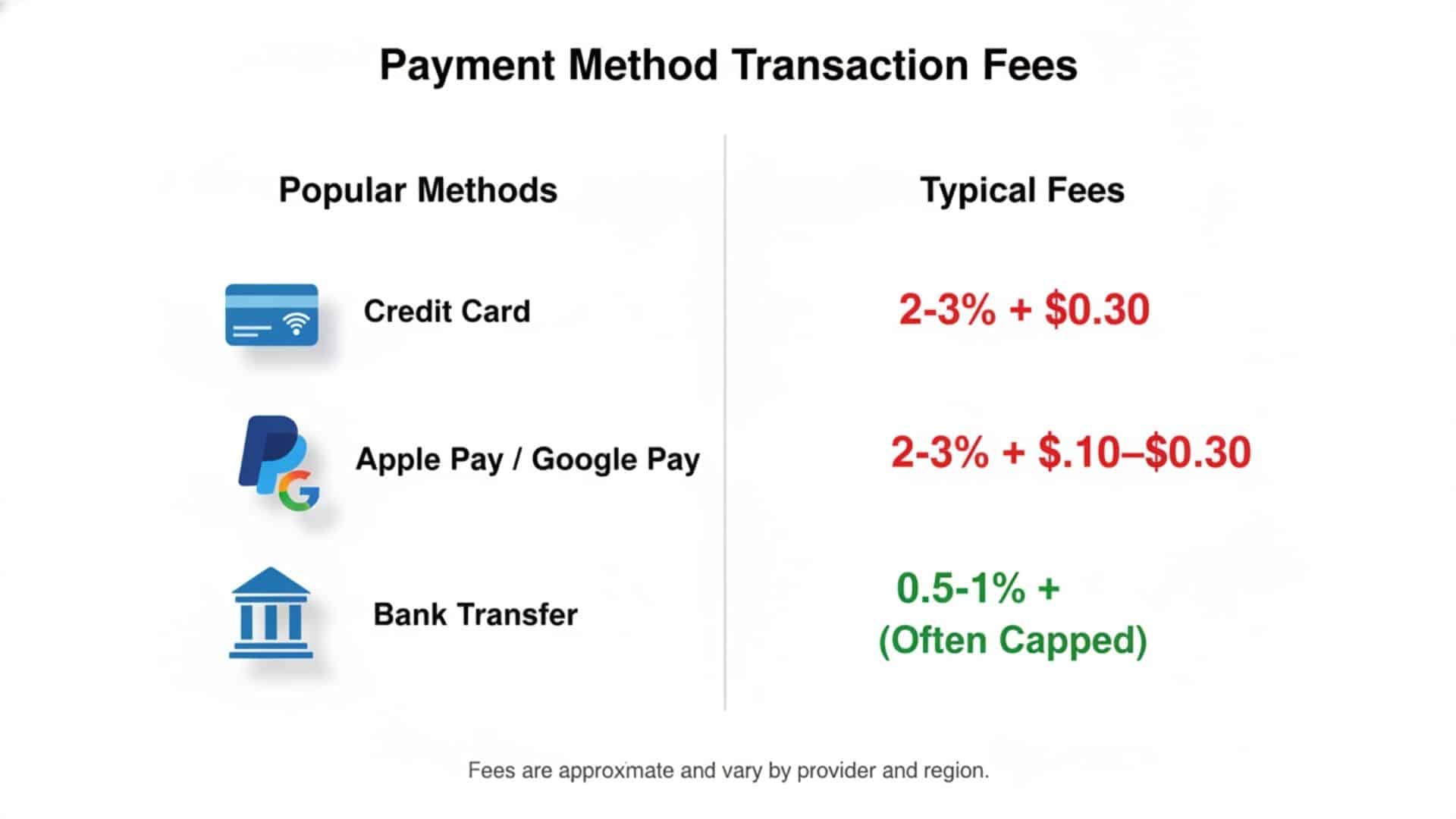

Best Online Payment Methods for Small Business

Each payment method serves a different purpose. This table provides a clear, side-by-side comparison to get you started with your research.

| Payment Method | Best For | Typical Fee | Settlement Time |

|---|---|---|---|

| Credit / Debit Cards | All business types | 2.5% – 3.5% per transaction | 1–2 business days |

| ACH Bank Transfer | B2B, services, high-ticket | 0.5% – 1.5% (often capped) | 2–4 business days |

| Digital Wallets (Apple Pay, Google Pay, PayPal) | Mobile and ecommerce | Similar to card rates | 1–2 business days |

| Buy Now, Pay Later (BNPL) | E-commerce, higher-ticket items | 2% – 8% per transaction | 1–3 business days |

| Online Invoicing / Pay-by-Link | Freelancers, service businesses | Varies by processor | 1–3 business days |

| Recurring / Subscription Billing | Memberships, retainers | Card or ACH rates apply | Per billing cycle |

- Credit and debit cards are the most widely accepted options. They work for nearly every business type and customer.

- ACH bank transfers cost less per transaction. They work especially well for larger payments where the fee savings add up fast.

- Digital wallets speed up mobile checkout. Customers skip entering card details, which reduces friction at the final step.

- Buy now, pay later can increase your average order value. The BNPL provider pays you upfront and collects from the customer over time.

- Online invoicing suits businesses that bill after completing work. You send a payment link, and the client pays on their own schedule.

- Recurring billing automates charges for subscription-based businesses. It reduces missed payments and manual follow-ups.

How Payment Processing Fees Work

Most businesses focus only on the transaction rate. But the full cost of accepting payments includes several fee types.

| Fee Type | What It Covers | Typical Range |

|---|---|---|

| Transaction Fee | Charged per payment | 0.5% – 3.5% + flat per-transaction fee |

| Monthly Platform Fee | Access to payment software | $0 – $50+ per month |

| Chargeback Fee | When a customer disputes a charge | $15 – $25 per dispute |

| Currency Conversion Fee | For cross-border payments | 1% – 3% added to transaction |

| Equipment / Integration Fee | Hardware or plugin setup | One-time or monthly |

To compare total cost, go beyond the headline rate. A processor charging 2.9% per transaction with no monthly fee may cost more than one at 2.4% plus a $25 monthly fee, depending on your sales volume.

Always calculate your actual monthly cost based on your average number of transactions and order value. This gives you a true comparison instead of a surface-level one.

Security, Compliance, and Fraud Prevention

A single data breach can cost a small business far more than any processing fee. Security should be part of your decision from day one.

PCI compliance is a set of rules that card networks require all businesses to follow. It covers how you store, process, and transmit card data. Most payment gateways handle PCI compliance through hosted checkout pages, so you never touch raw card data directly.

Key fraud prevention tools to look for in any payment provider:

- Tokenization: Replaces real card numbers with a code. Your system never stores sensitive data.

- Address Verification (AVS): Checks that the billing address matches the address on file for the card.

- 3D Secure: Adds a verification step during online purchases to confirm the cardholder’s identity.

- Real-time fraud monitoring: Flags unusual transaction patterns before they become losses.

| Chargebacks happen when a customer disputes a charge. They cost you the transaction amount plus a dispute fee. Using clear billing descriptions, maintaining delivery proof, and enabling verification tools all significantly reduce your chargeback exposure. |

How to Choose the Right Online Payment Methods for Your Small Business

The right payment setup depends on your customers, your margins, and how you sell. Use this framework to guide your decision.

- Start with your customers. Find out how they prefer to pay. Mobile-first customers expect digital wallets. Business clients often prefer ACH or invoice-based payments.

- Look at your average order value. For transactions above $500, ACH fees are often much lower than card fees. For smaller everyday purchases, card or wallet payments are more practical.

- Think about payout timing. If cash flow is tight, card payments settle more quickly than ACH payments. Factor that difference into your planning.

- Check your integrations. Your payment system should connect directly with your accounting software, ecommerce platform, or CRM. A mismatch creates manual work and room for errors.

- Growth plan. If you expect to sell internationally, choose a processor that supports multiple currencies from the start. Switching processors later is costly and time-consuming.

Common Mistakes Small Businesses Make With Online Payments

Avoiding these errors can save you money and prevent missed sales down the line.

- Too few payment options: Limiting customers to a single payment method reduces conversions. Offer at least two to three options at checkout.

- Choosing only on price: The cheapest processor is not always the best. Look at support quality, uptime, and fraud tools alongside fees.

- Ignoring mobile checkout: More than half of online purchases now occur on mobile devices. A poor mobile experience directly costs you sales.

- Skipping fraud protection: Not setting up basic fraud tools leaves your business open to chargebacks and financial loss.

- Missing recurring billing support: If you plan to offer memberships or retainers, confirm your processor supports it before signing up.

- Tools that do not connect: A payment system that does not integrate with your other software creates extra admin work and costly errors.

Recommended Payment Setup for Most Small Businesses

You do not need to offer every payment method. A focused setup that covers your core customer base is more effective.

| Business Type | Recommended Setup |

|---|---|

| New small business | Card payments + one digital wallet (e.g., PayPal or Apple Pay) |

| Service-based or freelance | Invoicing tool with card and ACH options |

| E-commerce store | Card, digital wallet, and BNPL (e.g., Afterpay or Klarna) |

| Subscription/membership | Recurring billing via card or ACH with automated retries |

| B2B or international | ACH for domestic + multi-currency card support for global clients |

Start with the basics and add more methods as your customer base grows. Overloading your checkout with too many options can confuse customers just as easily as having too few.

Bottom Line

In summary, choosing the right online payment methods for a small business comes down to knowing your customers, understanding your costs, and picking tools that fit how you sell. Cards, ACH, and digital wallets each serve a different purpose.

Using a smart mix of all three gives you strong coverage without overcomplicating your checkout.

Security and compliance should never be an afterthought. A secure checkout builds customer trust and protects your revenue at the same time. Review your payment setup at least once a year as your business grows and customer habits shift.

What payment method do your customers ask for most often? Share your experience in the comments below.

Frequently Asked Questions

What is the Best Online Payment Method for A Small Business?

There is no single best option. Most small businesses benefit from accepting credit cards, at least one digital wallet, and ACH for larger transactions. The right mix depends on your customers and how you sell.

What is the Cheapest Way to Accept Payments Online?

ACH bank transfers typically carry the lowest fees. They work best for larger transactions. For smaller purchases, flat-rate card processors often keep total costs manageable.

How many payment options should a small business offer online?

Most experts suggest two to four options. Cover cards, a digital wallet, and a bank transfer option if you regularly handle larger transactions.